Electric Mobility in Your Neighborhood

The number of electric vehicles on the roads is still fairly low, falling far short of the German government’s targets for 2020. Nevertheless, there has been extraordinary growth in the uptake of e-mobility products.1

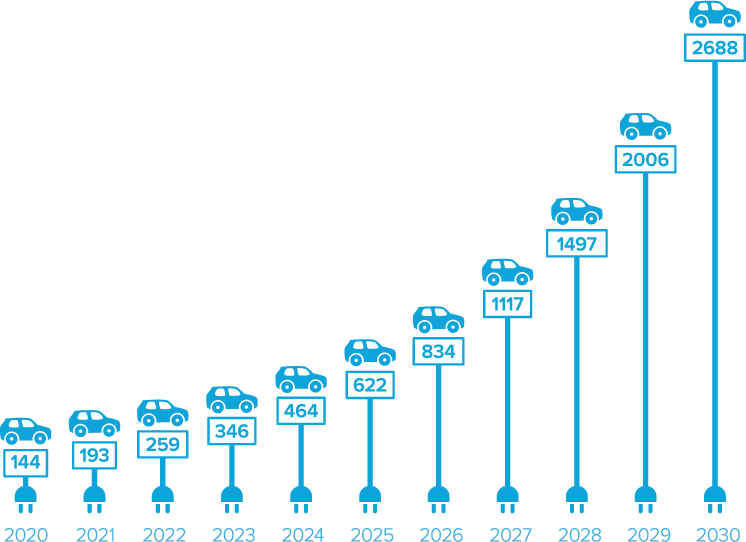

Fig. 1: Numbers are increasing: the ramp-up of electric vehicles on Germany’s roads, in thousand vehicles2

Based on the given forecast and looking at the example of a housing company with 30,000 households, the tenants would own almost 2,000 electric vehicles in the year 2030. This, coupled with the fact that the bulk of vehicle charging takes place at home,3 makes e-mobility a topic of increasing relevance for the housing industry. This kind of sector coupling between energy, mobility and housing is still not very well implemented and requires a large degree of coordination between the different players in order to be successful. Concrete results from research and practical application are still quite thin on the ground, which is why most of the projects implemented to date are pioneering.

There are numerous reasons why housing companies should address the subject of mobility. For one thing, quality of living in the apartments will be improved by the presence of adapted local mobility offers. And for another, increased property values can be achieved, as the expansion of mobility offers leads to better transport connections. Indeed, a housing company is in a good position to enter the mobility segment. That’s because the housing company knows their tenant clientele, can assess their mobility needs, and a large portion of a person’s mobility need is naturally linked directly to their place of residence – most journeys start or end at home, after all.

Technical and legal framework

The higher the charging capacity and the more charging points you make available on site, the higher the potential peak load will be. Since this can have a decisive influence on the overall capacity that needs to be provided and thus on the level of grid charges payable for a given neighborhood, there are a number of load management solutions already on the market. The aim of these is to cap any spontaneous load peaks by more evenly distributing the power that is being drawn over time. Such concepts are particularly interesting for fleet solutions when it does not matter which vehicle is used next, but applications on an individual basis are also conceivable. If the increased demand for power cannot be balanced out by load management, the building’s mains connection will need to be upgraded, a very cost-intensive undertaking.

When it comes to billing, there are two things to keep in mind. In every scenario where there can be more than a single specified customer using a given charging point, the customer or vehicle using the electricity must be identified. In addition, the complete process of payment and billing must be covered. From 2021 onwards, smart meters will also have to be installed.4

Business models

In the housing industry context, it is essential to choose a business model that can be realized with the amount of parking space actually present on the site. In other words, both the number of available parking spaces is limited and the location of these parking spaces is already predefined. The two most important criteria for categorizing business models are the number of parking spaces that will be fitted with charging points and who will be able to use these charging points.

- On the assumption that residents own (or will own) electric vehicles and charge their vehicles primarily overnight, it can make sense to equip private parking spaces with wallbox chargers providing up to 3.7 kW of power. This low charging capacity is often sufficient for a privately owned car – fully recharging the vehicle’s battery within the typical amount of downtime such a vehicle has.5 The advantages of this concept are that there is no need to set any rules for the use of shared charging points (e.g. “parking space must be vacated when charging is complete”). In addition, it makes billing easier, since each wallbox charger is assigned to a certain tenant and billing can take place through the tenant’s electricity bill. Finally, it can also be assumed that peak loads will tend to be low due to the charger’s low power rating. The disadvantages are that connection costs will be high due to the sheer number of wallbox chargers required and, at least in the next few years, the utilization and thus the economic efficiency of the chargers will be low. According to the ramp-up curve of demand, as illustrated above, approx. 6 % of the cars on German roads in 2030 will be electric vehicles.

- Offering a car sharing option is one way of making it easier to estimate the amount of electricity that will actually be consumed. Under this option, a small number of parking spaces are supplied with charging points. These charging points are not publicly accessible but supply vehicles docked at these locations and owned by a car sharing provider. Cooperating with a car sharing company that provides the vehicles and bills customers for the individual trips they take also keeps the total expenditure for the housing company low.

- Another model is to install a small number of charging points that all tenants (and possibly also non-residents) can use. The parking spaces in which the charging stations are installed are therefore not private but available for use by everyone. A higher power rating is required for such public charging points, as each will have to charge several vehicles per day. The advantage of this model lies in the higher level of utilization that will most probably be achieved by each charger, and also in the fact that it does not matter which tenants own or do not own an electric vehicle because charging points aren’t allocated to personal parking spaces.

Summary

By 2030, about 6 % of vehicles on the roads are expected to be electric. Housing companies will need to deal with this issue sooner rather than later, as the mains connections to residential buildings will need to be upgraded before too long. The business model involving charging points for mainly night-time charging is particularly relevant. This is a market that is evolving fast and dynamically. To be in a position to cope with the future growth in electric vehicles, it makes good business sense to start now, gathering experience with installing charging infrastructure and examining the impact it has on building connections or customers’ systems.

First standardizations have already been implemented, with the result that some uncertainties have been resolved. However, experience over a longer period of time is still lacking, meaning that no best practices are yet available.

Contact

Do you have questions regarding this topic? Please contact:

-

Dr. Mathias Hain

Dr. Mathias Hain

1Jahresbilanz des Fahrzeugbestands am 1. Januar 2018, Stand: 8. Mai 2018.

2 source: exponential function based on mean figures from various studies

3 Wietschel, Martin (2018): Empirische Erkenntnisse zur Nachfrage nach Ladeinfrastruktur und Optionen zur Lösung des Reichweitenproblems, Berlin, Germany, Stand: 03.08.2018

4 Klebsch, Wolfgang (31.08.2017): Ad-hoc-Laden und spontantes Bezahlen. Wie sich „punktuelles Aufladen“ umsetzen lässt, Frankfurt a.M., Germany, S. 78, Stand: 8. Mai 2018.

5 Many suppliers on the market already offer wallbox chargers at comparable prices with up to 22 kW charging capacity.