Direct Sales of Decentrally Generated Electricity with the Direct Electricity Supply Concept

What exactly is the direct electricity supply concept?

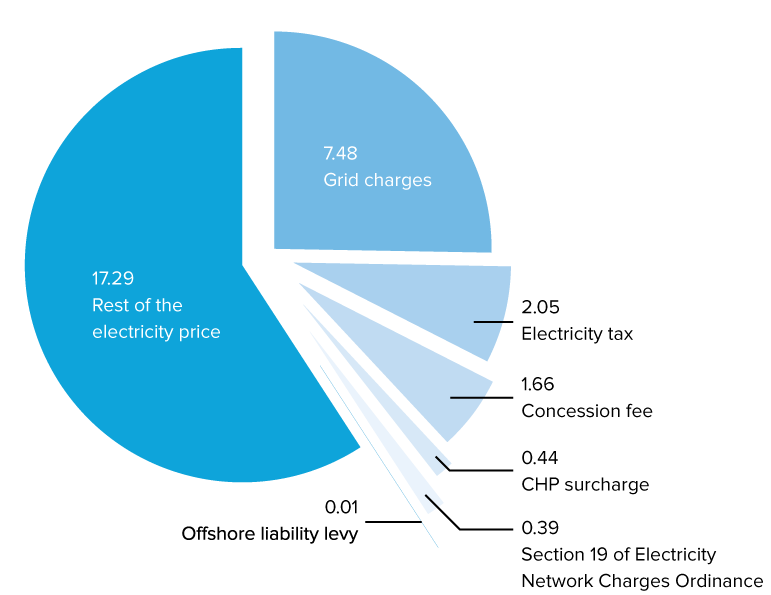

Known in Germany as Mieterstrom, the concept involves electricity being generated locally and delivered straight to end users in the neighborhood. Any electricity that is surplus to local needs is fed into the grid and corresponding payment is received; any extra electricity required is drawn from the grid. The advantage over feeding all of the locally generated electricity into the grid lies in the fact that it does not need to be transmitted through a grid or network (apart from the one inside the building), which means that the electricity price can be lower because various taxes, levies and charges are no longer incurred. These are, specifically, the concession fee, electricity tax, grid usage fees, CHP surcharge, interruptible load levy, Section 19(2) of the Electricity Network Charges Ordinance (Strom-NEV) and the offshore liability levy.1 These elements make up an average of 41 % of the domestic electricity price, though there are significant regional differences.2

Fig. 1: Electricity price breakdown in cent/kWh

Even before the law on direct electricity supply came into force in July 2017, electricity was already being sold through direct supply. However, as “direct supply” is not a protected term, it has been interpreted in different ways. As a result, many direct electricity supply projects have been implemented with photovoltaics (PV) only, or with combined heat and power (CHP) units, or even as a combination of both.

Parameters and implementation

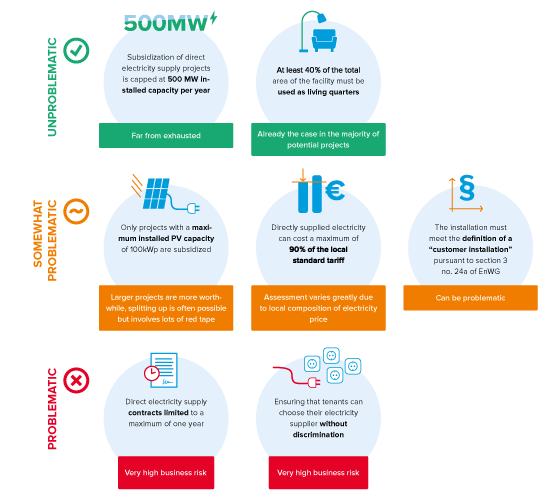

Projects of that kind can still be implemented since the law came into force, but it is now possible to have a building’s direct electricity supply subsidized by the state under certain circumstances. Subsidies depend on the size of the power-generating system and amount to 1.71–3.30 cents/kWh as of December 2017.3 However, this subsidy for decentralized electricity generation is subject to certain conditions: only PV systems are subsidized (i.e. no CHPs), and only up to a power output of 100 kWp. The electricity may not be fed through other grids and the system must meet the definition of a customer installation according to Section 3 No. 24a of the Energy Economy Law (EnWG). The facility within which the direct electricity supply is sold must be at least 40 % living quarters, which means that buildings used purely for commercial purposes are not covered. Each individual consumer must still be free to choose their electricity supplier without discrimination in order for the subsidy to be approved. The maximum term of any contract for direct electricity supply is one year. Furthermore, the price for the subsidized direct electricity supply is capped at 90 % of the local standard tariff. Last but not least, the legislator has limited the total number of subsidized projects to a maximum output of 500 MW per year, but it does not currently look like this limit will be reached in the foreseeable future.4

Fig. 2: Evaluation of the requirements arising from the law on direct electricity supply

The price cap of 10 % below the standard tariff appears easy to realize given the above-mentioned levies that do not need to be charged. However, there are some risks involved in implementing a direct supply project. The first is the fact that the requirement for the consumer to be able to choose their supplier without discrimination means that the project developer cannot be certain how many tenants will actually sign up for direct electricity supply, in other words cannot be sure what penetration rate they will achieve. Since selling electricity direct to tenants brings in more money than feeding it into the grid, the penetration rate is an indicator of great relevance for overall project profitability.5 Particularly when the project is being installed in an existing building (i.e. not a new build), it may be difficult to achieve a high enough penetration rate. That’s because of the high acquisition costs per customer, which must be covered by the electricity price. In addition, there are high billing costs.6 Closely connected to billing is the question of meter management within the system. When electricity is purchased in the standard way, the grid operator is responsible for providing and reading the electricity meter. Within a customer installation this responsibility falls to the operator.

Roles in project implementation

Apartments eligible for a direct electricity supply project are usually owned by a cooperative or a housing association. One possibility is for this company to handle all of the tasks itself. Normally they will need to build up the right expertise to do this, but on the other hand all of the profits will stay in-house. There is one big obstacle to this model, however: companies in the housing industry often take advantage of an extended reduction in trade tax. But the sale of electricity is considered a “harmful activity” in this context, which means that these tax concessions no longer apply – not only to the sale of electricity but to the company’s entire revenue (in the case of cooperatives, only above a certain percentage of revenue received from the sale of electricity). This means that it only makes sense to implement a direct electricity supply project for companies that no longer benefit from this tax break.

That said, this problem can be avoided if the housing company does not act as the company selling the electricity. It can either outsource this activity to a subcompany or collaborate with a contractor.

Profitability

As the large number of influencing factors already suggests, the profitability of direct electricity supply projects is highly dependent on individual circumstances. An expected project return is 5–7 % (4 % if all of the electricity is fed into the grid).7 However, this is very much project dependent, meaning that direct electricity supply projects are not worth implementing in many cases, which is also reflected in practice.89 One of the biggest influencing factors is the regional level of grid fees and thus also the concession fee, which is a percentage thereof. These two items alone result in around 8 cents/kWh in indirect subsidization owing to the fact that these fees are not payable. In addition, larger projects are often more profitable, which can make the combination of the 90 % rule with the 100 kWp limit problematic.

Summary

The study examines which factors affect the profitability of direct electricity supply projects, which is highly dependent on individual circumstances. The influencing factors examined are installed PV capacity, size of interim storage facilities, penetration rate and roles in the implementation of the project. Ideally, tenants should be able to purchase low-cost renewable electricity generated on their own rooftops and thus contribute to the energy transition.

The funding restrictions are still extensive and particularly restrict the implementation of more profitable (i.e. larger) projects. There are also a number of uncertainties associated with the organizational aspects of such a project. Within the first year of direct electricity supply being subsidized, the number of applications is still limited – confirmation that the obstacles mentioned are a concern. Tax implications for housing companies continue to ensure that implementation does not add value for a significant proportion of owners of buildings that may have the potential for direct electricity supply projects. A quick check can help to identify the key issues for your company and to find ideal locations for direct electricity supply projects in your portfolio.

Contact

Do you have questions regarding this topic? Please contact:

-

Dr. Mathias Hain

Dr. Mathias Hain

1 Ahlers/Kaspers (2017), p. 173

2 BDEW (January 9, 2018), p. 7

3 BNetzA (2017), p. 6

4 BNetzA (2018)

5 Hanusch/Hümpfner (2017)

6 Sagmeister (2017)

7 BMWi (n.d.), p. 4

8 BH&W and others (2017), p. 94

9 Konstantin (2009), p. 184