PropTech – The Real Estate Industry in Transition

The real estate industry has historically tended to be a conservative sector characterized by very gradual evolution.

Yet technological developments and the billions lying unused in the offers of property market leaders could set off a potential wave of innovation.1

The industry has recognized the signs of the times and is discussing the potential for cooperation between the old and new economy. A word that often crops up in this context is PropTech, which stands for property technology and describes digital products for the real estate sector. Events on this topic are offered regularly, including the MIPIM PropTech Summit on October 11, 2017 in New York and FUTURE: PropTech on September 14, 2017 in Berlin.

But what exactly is PropTech? This article illustrates the different segments that digital solution providers are split into and explains their importance for the real estate sector.

PropTech & friends

For some years now, FinTech has been one of the most frequently used words in the financial world. Not a day goes by without a new business idea coming out. FinTech (financial technology) is the name given to companies developing innovative business models for the financial sector. These include technologies like online payment systems, crowdfunding, financing platforms and online stock exchanges. As such, FinTech companies rarely offer dedicated solutions for the real estate industry (with the exception of things like crowdfunding for real estate projects). And yet there are some overlaps between FinTech and PropTech.

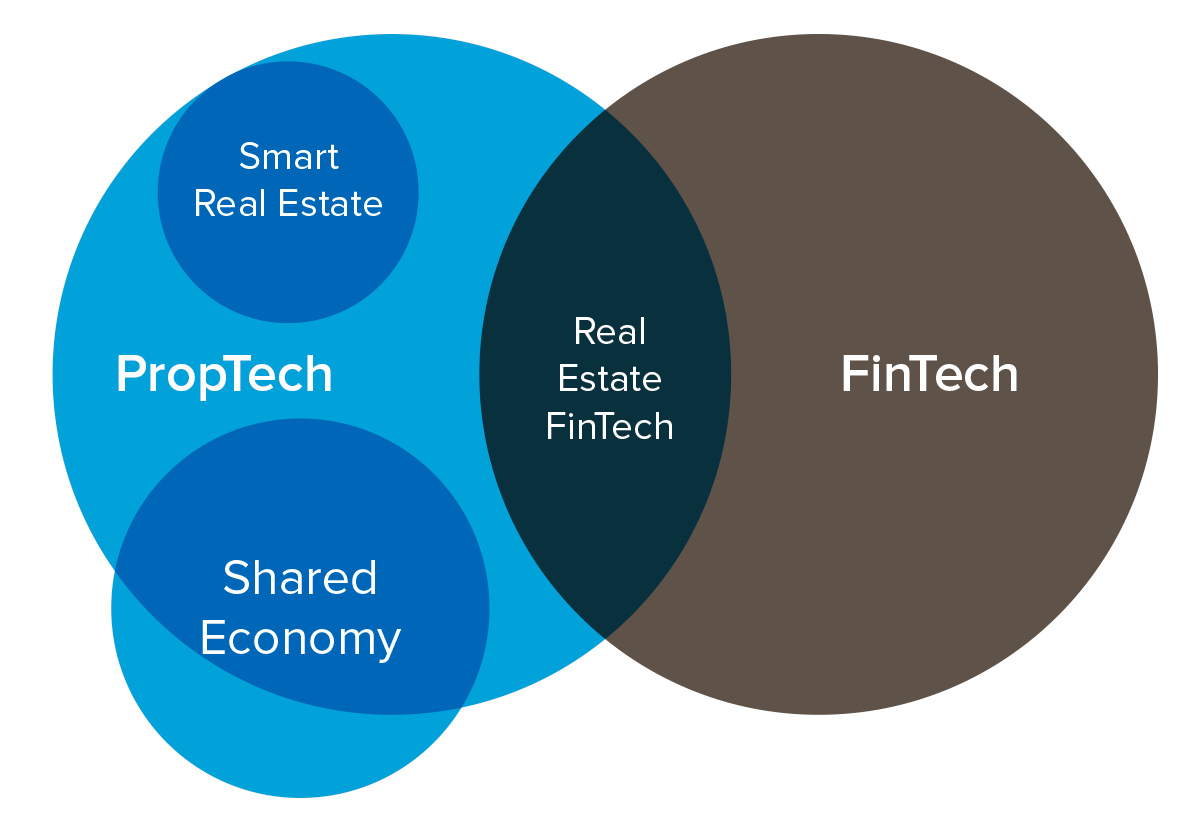

Figure 1: Differences and overlaps between PropTech and FinTech

The Venn diagram2 in Figure 1 shows real estate FinTech as a hybrid of FinTech and PropTech, whereas smart real estate and shared economy are largely or completely separate from FinTech and represent (pure) PropTech areas. In order to facilitate a better understanding of the individual areas, a brief summary and definition of each of the three categories is given, followed by a detailed consideration of real estate FinTech, smart real estate and shared economy. The main aim here is to examine the possible innovations and changes that lie in store for the real estate sector.

Real Estate FinTech refers to software-based platforms that optimize the buying and selling of real estate assets. Such assets may be classic (individual) properties or fund shares, or they may be debt and/or equity capital invested in real estate. Platforms may be limited to the provision of information, or they may also include the entire sale/transfer process.

Smart Real Estate is about software-based platforms that facilitate the running and management of real estate properties. The platforms may contain information on (individual) properties or entire cities. Advanced smart real estate platforms already enable the active management and control of real estate portfolios. Such platforms are mainly there to support asset, property and facility managers in their day-to-day business.

Shared Economy Real Estate describes software-based platforms that facilitate the daily use of real estate properties. Shared economy solutions deal mainly with usable space and buildings, including offices, logistics, apartments, etc. Here, too, the spectrum ranges from pure provision of information to active management of rental or transaction payments. These platforms focus on the active use of the real estate by residents/tenants.

At this point, we would like to point out that we will not be looking at ConTech (construction technology) in this article. Although some studies consider ConTech to be an offshoot of PropTech and the connection between the two a natural transition, we view them as adjacent areas instead. We don’t believe it is necessary to describe ConTech in detail in order to develop a full understanding of PropTech itself.

Real Estate FinTech

Classic FinTech and real estate FinTech are both primarily concerned with the support and realization of transactions. In contrast to classic FinTech, which deals with trading in financial products, real estate FinTech is all about trading in real estate. Above all, the very varied and widespread demand for housing combined with the diverse yet opaque supply situation offers huge potential for greater efficiency. There is currently no effective mechanism in place to bring supply and demand together. On the contrary, the numerous independent real estate agents benefit from the asymmetric distribution of information: brokers have no interest in sharing their market knowledge publicly. Due to the considerable size of individual transactions, they can still generate a high level of profits with a small number of transactions. However, there are already some companies striving to put an end to the asymmetric distribution of information by making information available to the public. The American Zillow Group, founded in 2006, for example, offers consumers the possibility to obtain information on property listings through its website without using the services of a real estate agent.3 Zillow Group does still cooperate with brokers and sends them promising properties direct. Nevertheless, such providers are helping break up the established asymmetric information situation in the real estate sector long term.4 Trulia (also part of the Zillow Group), Rightmove and Zoopla as well as ImmobilienScout24 are further examples of real estate FinTech information providers in the USA, the United Kingdom and Germany that are expected to precipitate a reduction and consolidation of traditional real estate agents.

According to Savills and the World Bank, the global real estate market is worth some USD 217 trillion, 75% of which is locked up in home ownership. Annual buying and selling of real estate in 2007 amounted to approximately USD 683 billion and rose to around USD 900 billion in 2015.5 This represents an annual trading volume of about 0.3–0.4% of the total property stock. The global real estate portfolio represents more than half of all established assets, but is also very illiquid. This estimate disregards the average additional costs of 3–6% for a transaction, including fees, brokers, due diligence, contracts, legal valuations and advisor’s fees (excluding taxes and failed transactions).6 Jeremy Sicklick, co-founder and CEO of San Francisco firm HouseCanary, also found that it takes an average of 100 days for a property in the US to change hands.7

In a market calculation, if we assume incidental transaction costs of, say, 4–5% for the annual trading of approx. USD 1 trillion of the global real estate portfolio (approx. 0.4% of the total market of USD 217 trillion) the resulting market volume comes out at USD 40–50 billion. This market is currently shared by advisors, real estate experts, lawyers and accountants. Should the real estate FinTech industry be able to make real estate trading “just” 10% more efficient, this would immediately reveal another USD 4–5 billion in potential returns. This calculation is enough to highlight the immense potential for the real estate FinTech sector and any companies that manage to establish themselves as first movers here. Furthermore, the calculation completely ignores the potential inherent in rising transaction volumes owing to declining illiquidity and faster transactions (<100 days). According to a forecast by Catella, the annual volume of transactions on the European residential property market is currently already growing at more than 5%, from EUR 37 billion in 2016 to EUR 39 billion in 2017.8 Reasons for this growth include urbanization, capital availability, migration and demographics. However, if better and more transparent transaction management combined with lower costs as a consequence of the reasons mentioned above led to a higher annual trading rate, the result would be further multi-billion euro growth in the real estate FinTech industry.

Smart Real Estate

What exactly are “smart” buildings? Smart buildings combine their historical purpose of providing space for their residents/users with the integration of new technologies to increase efficiency, e.g. in regulating the heating of the space. For the top five S&P 500 companies by market cap in the third quarter of 2016 – Apple, Alphabet (Google), Microsoft, Amazon and Facebook – this is already a decisive factor in the selection/optimization of their properties.9 What all five companies have in common is their need for huge amounts of energy to provide their services. The growing dominance of cloud computing, for example, compels Facebook to build enormous data centers with fiber optic networks that require functional access to large amounts of electricity.10

Furthermore, a smart building includes the sustainable use of input resources (water, air, energy) and a conscious and responsible approach to output resources (waste water, emissions). The expectations of users and investors with regard to the costs and functional aspects of smart buildings have changed significantly over the last 10-15 years. In the past, the traditional lease agreement between owner and user was dominated by the rent for the space itself, with utility costs being more the responsibility of the tenant/user. Owing to the increased demands of tenants/users and the innovations within smart buildings, the responsibility for optimized property management is gradually being shifted to the owner/manager of the property.11

All the values measured in a smart building can be read off conveniently and in real time via PCs, tablets and smartphones. Not only does this improve the user’s awareness of what they are consuming, it can also be used to control the building infrastructure more efficiently. Google already bought into this growing market in 2014 with the acquisition of Nest (producer of smart thermostats).12 Two years later, Apple launched a smart home ecosystem called Apple Home as part of its iOS 10 system. The aim with Apple Home was to establish it on the integrated home speaker market as a competitor to Amazon’s already successful Alexa technology.13 These products make it clear that smart building technology has long since arrived in the consumer’s living room and is no longer only of interest to industry. METR Building Management Systems GmbH is one of the latest examples of the growing relevance of smart buildings in Germany. METR GmbH achieved a top five ranking in the first “Smart Up the City” innovation award created in 2017 by Berlin-based residential construction company degewo AG.14 METR GmbH is laying the foundations of a digital infrastructure for residential and public buildings by connecting all of the intelligent devices and technical systems in a bid to make buildings smarter.

Despite these significant steps toward smart buildings, smart real estate is still in its infancy. Most of the existing residential buildings were built without any thought to the integration of technology, and the modernization process will take years to complete. However, there are also factors that may allow for a faster development of the smart real estate sector. On the industrial level, for example, the incumbent electricity suppliers can hardly keep up with the rapidly growing energy demand emanating from data centers and new developments will be absolutely crucial.15 In addition, more and more companies are committing themselves to reducing their carbon footprint, such as Facebook, which has announced plans to operate all of its business locations 100% from clean and renewable energy sources.16 This yields enormous growth potential for companies with innovative ideas to increase efficiency and could help the segment evolve faster. At the same time, private tenants are becoming more and more open to new technologies and are loving the possibilities they have of controlling, optimizing and ultimately reducing their consumption via their smartphones. In the future, smart real estate could even help optimize entire neighborhoods, including schools, libraries, hospitals, power plants, etc. Maalka is a company that is already working to make the Japanese district of Kashiwa-no-ha in Chiba Prefecture and Pearl District in Portland, Oregon, USA, more sustainable and environmentally friendly through smart real estate technologies.17

Shared EconomyReal Estate

As the name suggests, the shared economy in the real estate sector is primarily concerned with the sharing and/or joint use of real estate via technical platforms. The best known flagships in the real estate sector are Airbnb and WeWork. The American Airbnb platform deals with the booking and rental of private accommodation and currently has over 4 million advertisements spanning more than 190 countries (as of September 2017).18 The WeWork platform, also from the USA, provides shared workspaces, a community feel and services for entrepreneurs, business founders, freelancers, start-ups and small businesses. WeWork is currently valued at around USD 20 billion and manages approximately 10 million square meters of office space.19

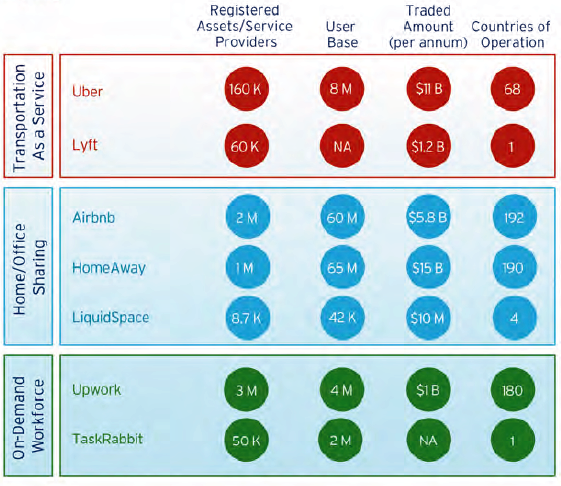

Yet the shared economy is not exclusive to the real estate sector. It is also strong in other areas such as transportation and the on-demand workforce. Since the turn of the millennium, the concept of the shared economy has met with increasing success. In the intervening years, the sector has produced ten unicorns (startups valued at USD 1 billion or more). These unicorns have decisively shaped their industries through innovations and business process transformation in recent years.20 The best known companies in the transportation sector are Uber, Lyft and Zipcar, while TaskRabbit and Upwork are among the biggest names facilitating the on-demand workforce, as illustrated in Figure 2. A recently published study by Jones Lang LaSalle (JLL) spelled out the strength of the trend toward the shared economy in figures. And in 2016, 74% of respondents in a JLL poll identified “thinking, talking and brainstorming as creating the most value within an organization.”21 For this reason, companies are implementing more and more alternative workplace solutions, e.g. cooperative working to increase collaboration within the company.

Figure 2: Selected companies in the shared economy

However, returning to the shared economy in the real estate sector, it is easy to see why this segment, especially the P2P (peer to peer) part of it, is growing significantly and is extremely attractive to startups and other innovative companies. Real estate is a capital-intensive investment whose prices have risen considerably in recent years. Minimum equity ratios of 10–30% of the transaction value, including fees and taxes, may be customary but they are almost impossible to finance for millennials. This is not just a German problem. Although London has seen 30,000 new apartments built since 2008, real estate prices have risen by around 60%. The typical minimum equity stake of 20% for an average house comes in at over GBP 100,000.22

The widening gap between rich and poor and the growing discrepancy between housing supply and demand in conurbations such as Germany’s seven largest cities is forcing millennials and other social groups into shared housing. The shared economy platforms they are using to rent increasingly scarce housing are benefiting from the growing demand. For years, growth on the supply side has been significantly lower than on the demand side. This imbalance in supply and demand is what led to the founding of Airbnb in the autumn of 2008. Founders Brian Chesky and Joe Gebbia, both of whom were unable to find a job after graduating from Rhode Island School of Design during the financial crisis, put up three guests on airbeds in their home during a design conference to earn some extra money. Years later, Airbnb already has over 4 million advertisements online and has cost the hotel industry about USD 450 million in lost revenue.23

Finally, we must also mention the growing importance of the “third place” in the shared economy. Examples of third places are cafés, clubs, libraries and parks. The third place is clearly differentiated from the first place (home) and the second place (workplace). Based on findings from the JLL study (2016),24 an average employee spends 25% of their time in third places. Modern employers are keen to try to move employees from second places to third places in order to increase collaboration, stimulate knowledge sharing and enhance the overall employee experience. Above all, the ever-changing nature of modern work and the importance of creative and innovative ideas have led to the continuous growth of third places globally. Shared economy platforms such as WeWork benefit significantly from this global trend.25 The German headquarters of PwC is a first mover here, having developed an app that encourages employees to spend more time together in third places. The app, known as “clapp – creative lunch app”, which is still being beta tested, encourages employees from different departments to have lunch together. Developed by the in-house innovation department dubbed the Experience Center, the app aims to increase knowledge sharing between different teams within PwC and to break open corporate silos.26

Conclusion

Despite being generally slow to embrace change, the real estate industry can no longer shut itself off from fundamental technological innovations. Although individual areas such as the housing industry have so far been spared the effect of disruptive business models, companies such as Zillow, Airbnb and WeWork prove that the impact of such business models can be huge. Different market players will need to address the issues in their own individual way. But the basic principle applies to everyone: All companies will need to keep an eye on the direction the market is going in and develop early strategies to implement the latest innovations within the organization in a structured manner.

Contact

Do you have questions regarding this topic? Please contact:

-

Dr. Mathias Hain

Dr. Mathias Hain

1 University of Oxford (2017): PropTech 3.0: the future of real estate

2 Venn, John M.A. (1880): On the Diagrammatic and Mechanical Representation of Propositions and Reasonings

3http://www.zillowgroup.com/abo... Retrieved September 20, 2017

4 University of Oxford (2017): PropTech 3.0: the future of real estate

5 ibid.

6 ibid.

7 ibid.

8 Wachstum auf europäischen Wohnungsmärkten [growth in Europe’s housing markets], Immobilien Zeitung, September 2017

9https://www.cnbc.com/2016/09/23/amazon-climbs-into-list-of-top-five-largest-us-stocks-by-market-cap.html. Retrieved September 26, 2017, Source: Factset

10 University of Oxford (2017): PropTech 3.0: the future of real estate

11 Green Building Council (2015): The Business Case for Green Buildings

12 https://abc.xyz/investor/news/releases/2014/0113.html. Retrieved September 26, 2017

13 http://www.businessinsider.com/apple-home-app-wont-change-the-smart-home-market-2016-9?IR=T. Retrieved September 26, 2017

14 https://bbu.de/nachricht/42623. Retrieved September 29, 2017

15 University of Oxford (2017): PropTech 3.0: the future of real estate

16 https://sustainability.fb.com/clean-and-renewable-energy/. Retrieved September 26, 2017

17 University of Oxford (2017): PropTech 3.0: the future of real estate

18 Airbnb Fast Fact. Retrieved September 17, 2017

19 Hempel, Jessi (2017-09-06), https://www.wired.com/story/this-is-why-wework-thinks-its-worth-20-billion/. Retrieved September 17, 2017

20 Tune, J.K. (2015): The Sharing Economy Has Created 17 Billion-Dollar Companies and 10 Unicorns

21 Jones Lang LaSalle (2016): A New Era of Co-working, http://jll.co.uk/united-kingdo...

22 University of Oxford (2017): PropTech 3.0: the future of real estate

23 Mahmoud, A. (2016): The Impact of AirBnb on the Hotel and Hospitality Industry

24 Jones Lang LaSalle (2016): A New Era of Co-working, http://jll.co.uk/united-kingdo...

25 Huet, E. (2016): WeWork Turns to New Business Model for India Expansion

26 PwC NextLevel and Experience Center Tour, Frankfurt am Main am 28. September 2017