How Residential Real Estate Companies Can Extract Value from the Homecare Market

Residential real estate companies today are subject to a diverse range of trends in a changing market. On the meta-level we have demographic change, bringing an aging and indeed shrinking society coupled with a rise in migration.

-

Dr. Mathias

Hain

Then there is the general urbanization trend causing substantial growth in the scale of our cities. The top-heavy age pyramid present in our society today and the fact that old people want to stay living in their familiar environment for as long as they can are two factors that place our local authorities and residential real estate companies under considerable strain in terms of the issues with which they are compelled to deal. The challenge lies in providing sufficient living accommodation for the young who want to move to the city, and for the old who want to stay there. There is growing demand for alternative living concepts such as assisted living, senior living communities and multi-generational accommodation in which several generations live under one roof.

The homecare market

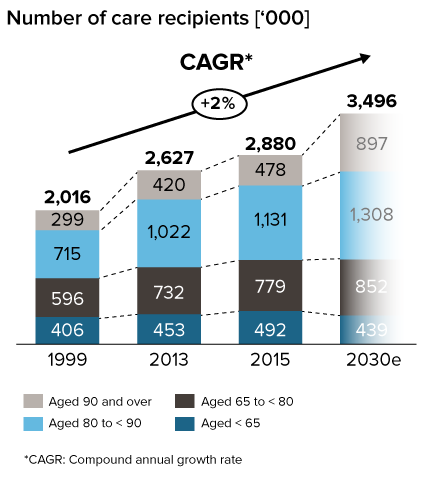

In 2015 there were some 2.9 million people in need of care1 in Germany. These people were looked after and cared for either in institutions (27%) or in their own homes (73%). The market for homecare in Germany is served by three types of organizations and accounted for revenue volume of 12.3 billion euros in 2015. The organizations involved are private companies, which make up 65% of the market, non-profit organizations (Caritas or Diakonie/church welfare) with 33% market share, and the public sector accounting for just 2% of the market. The number of care recipients is growing at a constant 2% p.a. And the proportion of people being cared for in their own home is set to rise disproportionately. Figure 1 illustrates the trend in recent years and the predicted development of the different age groups in the period through 2030.

Fig. 1: Development of care recipient numbers by age group

In Germany, the first, second and third act on strengthening long-term care (PSG, Pflegestärkungsgesetz I, II, III) and the rules laid down in the social security statutes, in this case social act five (SGB V – statutory health insurance) and social act eleven (SGB XI – long-term care insurance), form the legal framework within which homecare services are provided. There are five ‘care degrees’ (Pflegegrade): each care recipient is assigned one of them by their nursing care insurance fund. The care degree determines which services a person can access and how much of the cost will be covered by the nursing care insurance fund. Any services beyond this scope must be paid for by the care recipient themselves.

Providing in-home care services is very time consuming and labor intensive for care providers. The demand for qualified care workers is high, with many regions unable to meet the demand, at least in part. Care providers endeavor to make themselves attractive employers by making the working conditions as pleasant as possible by, for example, reducing driving time by optimizing carers’ route plans. Much of the work carried out by carers involves activities for which qualified personnel is not required. This includes help around the home, which is often done by auxiliaries or sometimes by members of the family.

Many providers of homecare services are keen to build their own facilities for assisted living or are taking steps to purchase and repurpose existing buildings. However, they often lack the funding to do this given that banks apply very restrictive financing conditions to such concepts or, more to the point, to such borrowers. That is because homecare services are in many cases still provided through sole proprietorships rather than limited liability companies. Assisted living as a concept does not in itself fall under the provisions for special buildings in the building regulations2, nor is it classified as a care home under the national or regional care home acts. In-home assisted living means that care recipients live in their own homes (an apartment with bathroom and kitchen) where they are cared for by family members or care facility employees. Care recipients are entitled to care aids to facilitate their care. The federal government subsidizes what it calls measures to improve the living environment (e.g. accessible bathrooms) to the tune of EUR 4,000 per measure, per care recipient. Senior living communities can also access this subsidy of EUR 4,000 per measure, per care recipient up to a maximum of EUR 16,000 per senior living community.

Working for or in an assisted living community is very attractive for care providers and their employees. For one thing, the care provider has better control over their costs as a result, and for another, the employees benefit from the elimination or minimization of driving time.3

Options that residential real estate companies can take

Residential real estate companies can increase their revenues by developing concepts to match their specific situation and tenant structure. There are numerous options for how to maintain a high occupancy rate long term and meet the needs of older residents and people in need of care who want to stay living in their familiar neighborhood for as long as possible. Besides cooperating with care providers, it could also be possible for residential real estate companies to set up their own care provider as a subsidiary or joint venture. The legal framework in Germany enables real estate companies to set up their own care facilities.

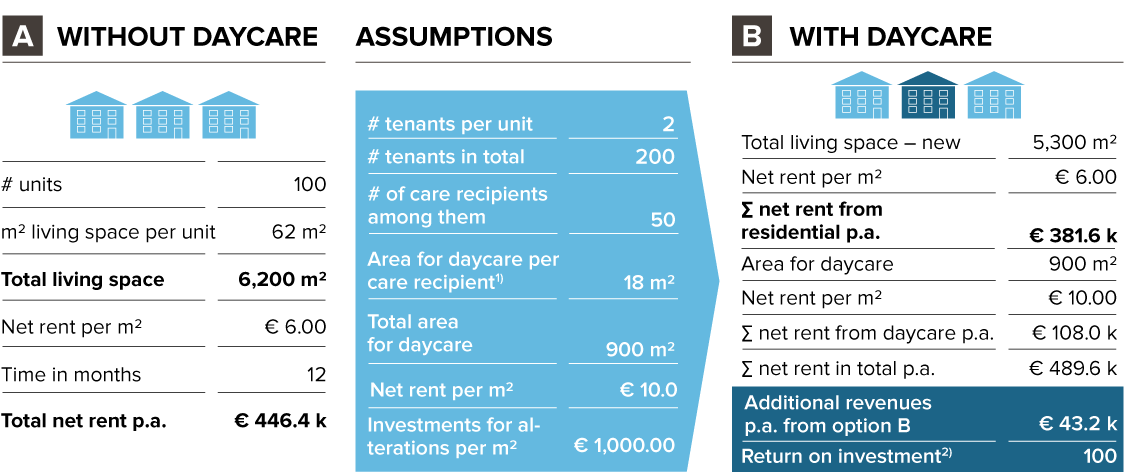

A first step toward approaching this subject would be too look for a suitable building and to create spaces in it which a care provider could use for daycare services. This would mean creating a communal lounge (a place for residents to socialize), including bathroom and kitchen facilities and integrating fire protection measures. Figure 2 illustrates the potential for a sample rental property of that kind.

Fig. 2: Sample ROI for a building with assisted living vs. traditional apartments

This example assumes that part of the original residential space is turned into space for daycare facilities. An area of around 18m² per care recipient is assumed in the calculations here. There is no statutory minimum but this figure is currently taken as the basis for new build projects of this kind.4 The residential real estate company can lease the 900m² of space allocated for daycare provision to a care provider (cooperation partner) at a higher net rent of EUR 10 per m² per month. This gives the real estate company an extra EUR 4 per m² per month in revenues compared to the usual net rent for residential units (EUR 6 per m² per month). On a yearly basis that amounts to an extra EUR 43,200 in revenues. This is offset by investment costs of around EUR 900,000, or EUR 1,000 per m². This results in an investment return of 4.8%,5 illustrating the potential that can be achieved by repurposing just 15% of the residential space (900 m²).

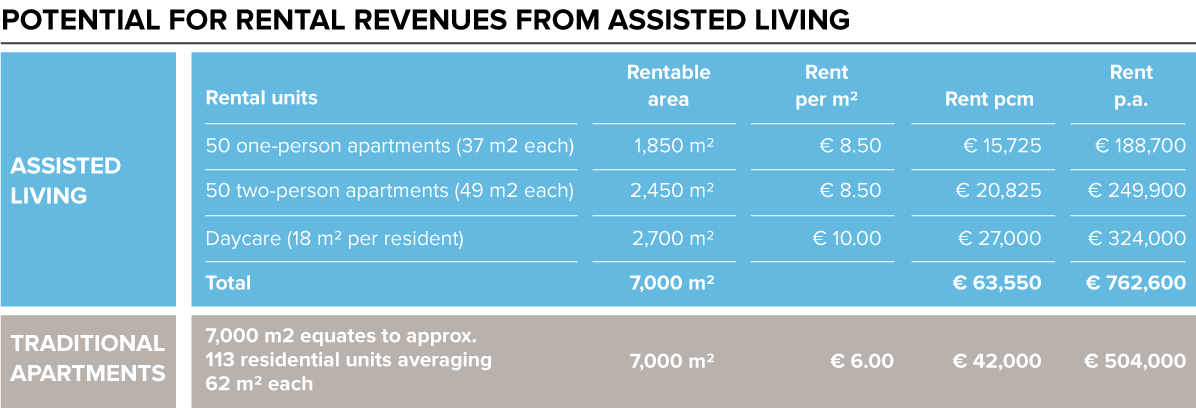

As mentioned above, care providers are very interested in creating their own assisted living facilities. The next example (see Fig. 3) shows the rental potential that a new build project for pure assisted living can have for a real estate company.

Fig. 3: New build project for assisted living accommodation vs. traditional apartments

The demand for accommodation in assisted living facilities has seen a rapid rise in recent years and is expected to increase further. Popular apartment sizes are from 34 to 42 m² for 1-room apartments and approximately 49 m² for 2-room apartments. Real-life examples show that higher net rents (from €2.50 per m² as in this example) can be achieved with assisted living facilities. If we include the income from the area used for the daycare services, rental income comes out more than 50% higher than it would have been for the same rentable area. Construction costs for the two variants are almost identical, given that this kind of assisted living facility is not subject to any special building regulations. The additional costs of installing extra fire protection measures in assisted living facilities are quickly recouped from the additional income generated.

These are two examples of cooperation, whereby a residential real estate company makes space or an entire building available and rents out a facility for use by a homecare provider.

In combination with the options listed above, there is another option for real estate companies, which is to establish or acquire their own homecare provider. On the one hand, this enables synergies to be realized between the companies in areas such as finance and accounting or IT. And on the other hand, homecare providers generate a proven EBT margin of 5 to 20%. An expert interview conducted by RITTERWALD in March 2017 found that as a rule of thumb, once a homecare business is fully up and running, 70 to 80% of revenues go on personnel costs and approximately 10 to 15% go on all other costs of materials. Which means that, if appropriately integrated into the residential real estate company’s corporate structure, a homecare service can makes good business sense as a complement to the company’s residential real estate activities.

Summary

This outline illustrates how residential real estate companies can meet the wishes of their tenants who want to stay living in their familiar environment in their old age. Depending on their buildings and their tenant structure, or when undertaking new builds, real estate companies should consider the potential value that could be added from alternative rental properties through the creation of space for daycare services or assisted living facilities. In the context of strategic neighborhood development with further synergies in mind, residential real estate companies could even go so far as to consider founding their own homecare provider as a subsidiary company. A sensible combination of the options described above holds out the best prospect of commercial success for real estate companies.

Create added value with RITTERWALD

RITTERWALD principally advises the real estate sector with a focus on corporate development and mergers & acquisitions. Our “Care” Team is composed of industry experts complemented by functional expertise on strategy, organization, digitization and M&A matters. If you have any questions or comments on this article or are interested in the topic of residential real estate companies or homecare services in general, we’d love to hear from you.

Contact

Do you have questions regarding this topic? Please contact:

-

Dr. Mathias Hain

1 Social act eleven of the social security statutes (SGB XI) defines the need for long-term care. Sections 14 and 15 contain the precise provisions defining when a person is considered “in need of care”. This determines the person’s entitlement to care services.

2 Please note that state legislation is authoritative and that it is important to check on a case-by-case basis which other regulations also apply.

3 See Section 40 of the social security statutes (SGB XI)

4 See journal “Häusliche Pflege” 01/2017

5 Please note that this is a periodic ROI, resulting in a payback period of about 21 years for the investment.